Frequently, the agricultural industry in Kenya remains vital, contributing 20 percent of the country's GDP and 27 percent indirectly through its connections with other sectors. Additionally, the sector employs more than 40% of the workforce overall and more than 70% of people living in rural areas.

Given the critical role the sector plays in providing livelihoods and food for the Kenyan economy, it is increasingly important to ensure that quality, high frequency data is available to inform the food security situation in the country, the prevailing prices and their expectations and the challenges that may affect agricultural production.

However, understanding the trends in Digital Finance Service (DFS) influence on the sector’s output is critical given the significant weight of food in the consumer basket, which depends on how much capital is channeled towards production.

In Kenya, for instance, digital finance for smallholder farmers is still in its infancy. The technology and the funding are available, but they haven't yet been integrated on a large scale.

Status of DFS

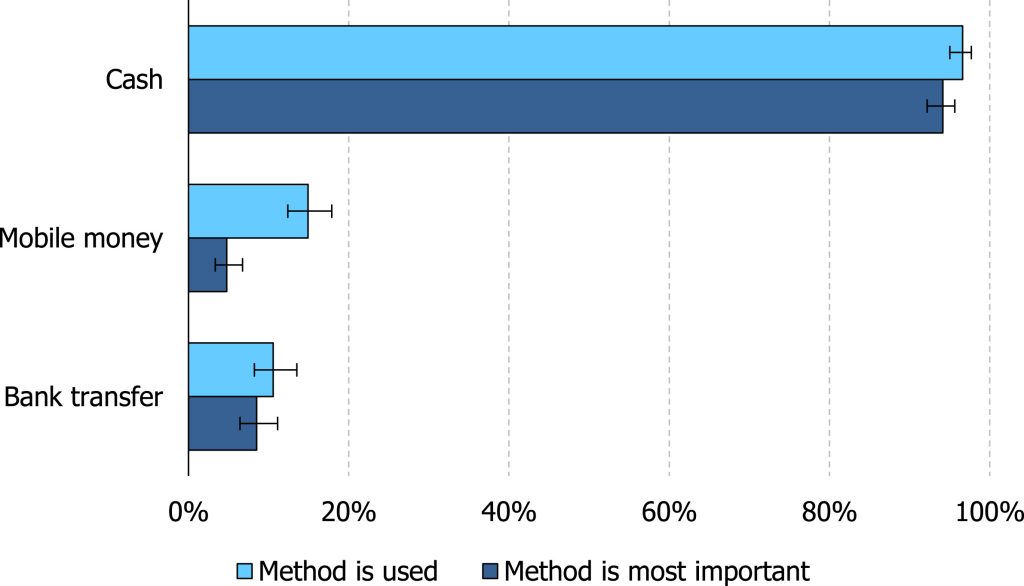

Financial services to smallholders specifically are still largely analog, though there are pockets of emerging digitization. Over 82% of farmers in Kenya already use mobile financial services (MFS) in general. However, fewer than 15% of the farmers use MFS for agricultural purposes. Fewer than 1% of the farmers have used mobile banking loans for agriculture (Martin et. al., 2021).

However, the use of cash is still widespread, particularly among rural residents where 50% of the population transacts using a combination of platforms, including cash, mobile money, and bank transfers.

This restricts the amount of data that is available for financiers to refer to when granting credits. The rendering of financial products and services is made more complex due to the relatively small size of transactions in money and the substantial risk that is endemic to smallholder agriculture.

Banks, which are the biggest lenders but are still cautious with agricultural finance and prefer to lend to established organizations that can put up the necessary collateral as compared to small-scale farmers. The Economic Survey 2019 shows that agriculture makes up only 3.6% of commercial banks' commercial lending portfolio.

On the other hand, the microfinance sector nevertheless remains in its infancy, having encountered trouble generating new clients and incurring yearly losses in the past few years.

According to World Bank's Digital Dividends Report, 2016, nearly 60 percent of the world’s population were still offline and could not participate in the digital economy in any meaningful way with agriculture looped in. Since then, the status has shifted to about one-third of the global population, or 2.6 billion people, remaining offline in 2023. The reduction from the estimated 2.7 billion people offline in 2022 leaves 33 percent of the global population unconnected in 2023. However, the benefits of digital technologies can be employed to offset the growing setbacks.

Fewer than 1% of the farmers have used mobile banking loans for agriculture.

Martin et. al., 2021

This potential has spurred several efforts in both the public and corporate sectors to develop digital tools, platforms, and architectures with the goal of significantly transforming agricultural markets.

DFS for agriculture has been affected by certain significant legislative obstacles that Kenya's financial sector has faced. The primary goal of government policy so far has been to shield customers from exorbitant interest rates, whether they are offered by banks or by mobile lenders.

Challenges

Digital tools, many of which emerge without sufficient understanding of local market constraints, pre-existing local information systems and networks, or how these systems and networks can be complemented or integrated with digital tools.

New information technologies may be foreign to farmers and other agents or disruptive to markets that were previously efficient under the constraints of existing institutions if contextual awareness is lacking.

Information asymmetries may cause skepticism about using DFS due to concerns about reliability, security and fraud.

High charges for accessing DFS can be prohibitive to smallholder farmers who are already facing financial constraints.

The scaling of many of the DFS tools is constrained by a lack of clarity on inclusion, or the provision of services to marginalized groups; smallholder farmers, women and youth farmers, and farmers in marginal agro-ecological zones.

Most of the formal finance for agriculture is likely to get into other buckets that are less likely to plough back interest for repayment or meet the intended impact.

Financial institutions have yet to use data, which has potential yet to be realized.

Keeping Pace with the Rapidly Evolving DFS

DFS improves the convenience of transactions between value chain actors, e.g., between farmers and traders, or between aggregators and processors. Many of these innovations aim to reduce the time, and risk associated with exchanges in imperfect or incomplete markets.

Many farmers not only require technical support to effectively use new agricultural inputs, but it is also in the best interest of the credit provider to ensure that farmer practices yield good results as loan repayment depends on it.

DFS needs to involve the targets in the product design and delivery by testing them first to realize success. Less than 10% of farmers are in formalized farmer groups within structured value chains, making human agents frequently necessary for the acquisition and screening of farmer groups.

There is a strong need to systematically capture scaling experiences – including failures – in order to better understand the critical features of viable scaling strategies in different contexts. The current lack of nuanced evidence from both successful and unsuccessful scaling efforts around agriculture-focused digital tools in Africa is impeding learning, which may guide future scaling efforts

Equally important are investments in intangible infrastructure such as agricultural data ecosystems that generate site-specific, spatially explicit crops, soil, land, weather, post/disease, and market data, and integrate these data with farmer registries, weather data, and other data streams.

References

- Central Bank of Kenya. (2023). Agriculture Sector Survey of May 2023.

- Martin C. Parlasca, Constantin Johnen, Matin Qaim. (2022). Use of mobile financial services among farmers in Africa: Insights from Kenya. Global Food Security Journal, Volume 32.

- Kenya National Bureau of Statistics. (2019), Economic Survey 2019.

- World Bank Group. (2016). World development report 2016: Digital dividends. World Bank Publications.

For more information, contact info@fspnafrica.org.